Page 30 - Policy Economic Report - December 2024

P. 30

POLICY AND ECONOMIC REPORT

OIL & GAS MARKET

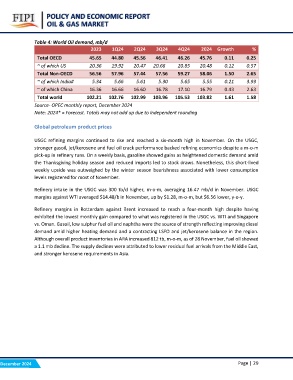

Table 4: World Oil demand, mb/d 2Q24 3Q24 4Q24 2024 Growth %

2023 1Q24

0.25

Total OECD 45.65 44.80 45.56 46.41 46.26 45.76 0.11 0.57

2.65

~ of which US 20.36 19.92 20.47 20.66 20.85 20.48 0.12 3.93

2.63

Total Non-OECD 56.56 57.96 57.44 57.56 59.27 58.06 1.50 1.58

~ of which India# 5.34 5.66 5.61 5.30 5.65 5.55 0.21

~ of which China 16.36 16.66 16.60 16.78 17.10 16.79 0.43

Total world 102.21 102.76 102.99 103.96 105.53 103.82 1.61

Source- OPEC monthly report, December 2024

Note: 2024* = Forecast. Totals may not add up due to independent rounding

Global petroleum product prices

USGC refining margins continued to rise and reached a six-month high in November. On the USGC,

stronger gasoil, jet/kerosene and fuel oil crack performance backed refining economics despite a m-o-m

pick-up in refinery runs. On a weekly basis, gasoline showed gains as heightened domestic demand amid

the Thanksgiving holiday season and reduced imports led to stock draws. Nonetheless, this short-lived

weekly upside was outweighed by the winter season bearishness associated with lower consumption

levels registered for most of November.

Refinery intake in the USGC was 300 tb/d higher, m-o-m, averaging 16.47 mb/d in November. USGC

margins against WTI averaged $14.48/b in November, up by $1.28, m-o-m, but $6.56 lower, y-o-y.

Refinery margins in Rotterdam against Brent increased to reach a four-month high despite having

exhibited the lowest monthly gain compared to what was registered in the USGC vs. WTI and Singapore

vs. Oman. Gasoil, low sulphur fuel oil and naphtha were the source of strength reflecting improving diesel

demand amid higher heating demand and a contracting LSFO and jet/kerosene balance in the region.

Although overall product inventories in ARA increased 812 tb, m-o-m, as of 28 November, fuel oil showed

a 1.1 mb decline. The supply declines were attributed to lower residual fuel arrivals from the Middle East,

and stronger kerosene requirements in Asia.

December 2024 Page | 29