Page 8 - Policy Economic Report_Mar'25

P. 8

POLICY AND ECONOMIC REPORT

OIL & GAS MARKET

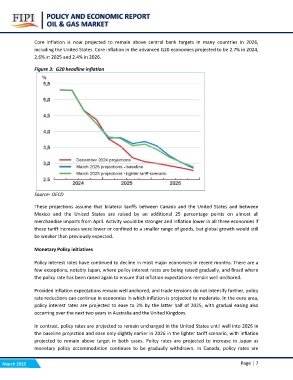

Core inflation is now projected to remain above central bank targets in many countries in 2026,

including the United States. Core inflation in the advanced G20 economies projected to be 2.7% in 2024,

2.6% in 2025 and 2.4% in 2026.

Figure 3: G20 headline inflation

Source- OECD

These projections assume that bilateral tariffs between Canada and the United States and between

Mexico and the United States are raised by an additional 25 percentage points on almost all

merchandise imports from April. Activity would be stronger and inflation lower in all three economies if

these tariff increases were lower or confined to a smaller range of goods, but global growth would still

be weaker than previously expected.

Monetary Policy initiatives

Policy interest rates have continued to decline in most major economies in recent months. There are a

few exceptions, notably Japan, where policy interest rates are being raised gradually, and Brazil where

the policy rate has been raised again to ensure that inflation expectations remain well-anchored.

Provided inflation expectations remain well anchored, and trade tensions do not intensify further, policy

rate reductions can continue in economies in which inflation is projected to moderate. In the euro area,

policy interest rates are projected to ease to 2% by the latter half of 2025, with gradual easing also

occurring over the next two years in Australia and the United Kingdom.

In contrast, policy rates are projected to remain unchanged in the United States until well into 2026 in

the baseline projection and ease only slightly earlier in 2026 in the lighter tariff scenario, with inflation

projected to remain above target in both cases. Policy rates are projected to increase in Japan as

monetary policy accommodation continues to be gradually withdrawn. In Canada, policy rates are

March 2025 Page | 7