Page 8 - Policy Economic Report - September 2024

P. 8

POLICY AND ECONOMIC REPORT

OIL & GAS MARKET

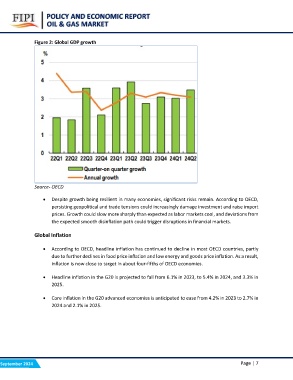

Figure 2: Global GDP growth

Source- OECD

• Despite growth being resilient in many economies, significant risks remain. According to OECD,

persisting geopolitical and trade tensions could increasingly damage investment and raise import

prices. Growth could slow more sharply than expected as labor markets cool, and deviations from

the expected smooth disinflation path could trigger disruptions in financial markets.

Global Inflation

• According to OECD, headline inflation has continued to decline in most OECD countries, partly

due to further declines in food price inflation and low energy and goods price inflation. As a result,

inflation is now close to target in about four-fifths of OECD economies.

• Headline inflation in the G20 is projected to fall from 6.1% in 2023, to 5.4% in 2024, and 3.3% in

2025.

• Core inflation in the G20 advanced economies is anticipated to ease from 4.2% in 2023 to 2.7% in

2024 and 2.1% in 2025.

September 2024 Page | 7