Page 37 - Policy Economic Report_Feb'25

P. 37

POLICY AND ECONOMIC REPORT

OIL & GAS MARKET

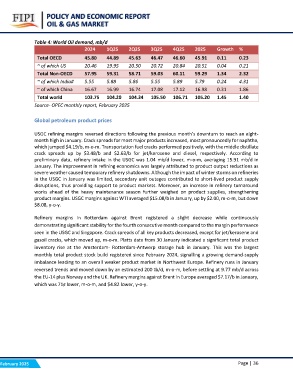

Table 4: World Oil demand, mb/d 2Q25 3Q25 4Q25 2025 Growth %

2024 1Q25 46.47 46.60 45.91 0.11 0.23

20.72 20.84 20.51 0.04 0.21

Total OECD 45.80 44.89 45.63 59.03 60.11 59.29 1.34 2.32

5.55 5.89 5.79 0.24 4.31

~ of which US 20.46 19.95 20.50 17.08 17.12 16.98 0.31 1.86

Total Non-OECD 57.95 59.31 58.71 105.50 106.71 105.20 1.45 1.40

~ of which India# 5.55 5.88 5.86

~ of which China 16.67 16.99 16.74

Total world 103.75 104.20 104.34

Source- OPEC monthly report, February 2025

Global petroleum product prices

USGC refining margins reversed directions following the previous month’s downturn to reach an eight-

month high in January. Crack spreads for most major products increased, most pronouncedly for naphtha,

which jumped $4.19/b, m-o-m. Transportation fuel cracks performed positively, with the middle distillate

crack spreads up by $3.48/b and $2.63/b for jet/kerosene and diesel, respectively. According to

preliminary data, refinery intake in the USGC was 1.04 mb/d lower, m-o-m, averaging 15.91 mb/d in

January. The improvement in refining economics was largely attributed to product output reductions as

severe weather caused temporary refinery shutdowns. Although the impact of winter storms on refineries

in the USGC in January was limited, secondary unit outages contributed to short-lived product supply

disruptions, thus providing support to product markets. Moreover, an increase in refinery turnaround

works ahead of the heavy maintenance season further weighed on product supplies, strengthening

product margins. USGC margins against WTI averaged $15.08/b in January, up by $2.00, m-o-m, but down

$8.08, y-o-y.

Refinery margins in Rotterdam against Brent registered a slight decrease while continuously

demonstrating significant stability for the fourth consecutive month compared to the margin performance

seen in the USGC and Singapore. Crack spreads of all key products decreased, except for jet/kerosene and

gasoil cracks, which moved up, m-o-m. Platts data from 30 January indicated a significant total product

inventory rise at the Amsterdam- Rotterdam-Antwerp storage hub in January. This was the largest

monthly total product stock build registered since February 2024, signalling a growing demand-supply

imbalance leading to an overall weaker product market in Northwest Europe. Refinery runs in January

reversed trends and moved down by an estimated 200 tb/d, m-o-m, before settling at 9.77 mb/d across

the EU-14 plus Norway and the UK. Refinery margins against Brent in Europe averaged $7.17/b in January,

which was 71? lower, m-o-m, and $4.82 lower, y-o-y.

February 2025 Page | 36