Page 30 - Policy Economic Report - November 2024

P. 30

POLICY AND ECONOMIC REPORT

OIL & GAS MARKET

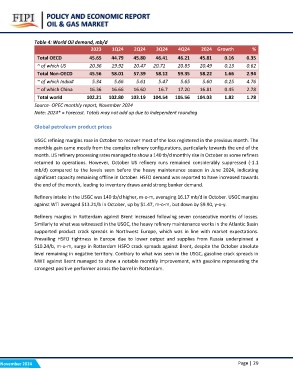

Table 4: World Oil demand, mb/d 2Q24 3Q24 4Q24 2024 Growth %

2023 1Q24

0.35

Total OECD 45.65 44.79 45.80 46.41 46.21 45.81 0.16 0.62

2.94

~ of which US 20.36 19.92 20.47 20.71 20.85 20.49 0.13 4.76

2.78

Total Non-OECD 45.56 58.01 57.39 58.12 59.35 58.22 1.66 1.78

~ of which India# 5.34 5.66 5.61 5.47 5.65 5.60 0.25

~ of which China 16.36 16.66 16.60 16.7 17.20 16.81 0.45

Total world 102.21 102.80 103.19 104.54 105.56 104.03 1.82

Source- OPEC monthly report, November 2024

Note: 2024* = Forecast. Totals may not add up due to independent rounding

Global petroleum product prices

USGC refining margins rose in October to recover most of the loss registered in the previous month. The

monthly gain came mostly from the complex refinery configurations, particularly towards the end of the

month. US refinery processing rates managed to show a 140 tb/d monthly rise in October as some refiners

returned to operations. However, October US refinery runs remained considerably suppressed (-1.1

mb/d) compared to the levels seen before the heavy maintenance season in June 2024, indicating

significant capacity remaining offline in October. HSFO demand was reported to have increased towards

the end of the month, leading to inventory draws amid strong bunker demand.

Refinery intake in the USGC was 140 tb/d higher, m-o-m, averaging 16.17 mb/d in October. USGC margins

against WTI averaged $13.21/b in October, up by $1.47, m-o-m, but down by $9.90, y-o-y.

Refinery margins in Rotterdam against Brent increased following seven consecutive months of losses.

Similarly to what was witnessed in the USGC, the heavy refinery maintenance works in the Atlantic Basin

supported product crack spreads in Northwest Europe, which was in line with market expectations.

Prevailing HSFO tightness in Europe due to lower output and supplies from Russia underpinned a

$10.24/b, m-o-m, surge in Rotterdam HSFO crack spreads against Brent, despite the October absolute

level remaining in negative territory. Contrary to what was seen in the USGC, gasoline crack spreads in

NWE against Brent managed to show a notable monthly improvement, with gasoline representing the

strongest positive performer across the barrel in Rotterdam.

November 2024 Page | 29