Page 34 - Policy Economic Report - August 2025

P. 34

POLICY AND ECONOMIC REPORT

OIL & GAS MARKET

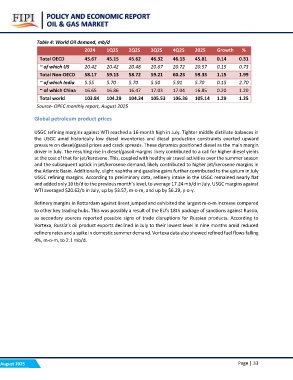

Table 4: World Oil demand, mb/d

2024 1Q25 2Q25 3Q25 4Q25 2025 Growth %

Total OECD 45.67 45.15 45.62 46.32 46.13 45.81 0.14 0.31

20.67 20.72 20.57 0.15 0.73

~ of which US 20.42 20.42 20.48 59.21 60.23 59.33 1.15 1.99

5.50 5.91 5.70 0.15 2.70

Total Non-OECD 58.17 59.13 58.72 17.03 17.04 16.85 0.20 1.20

~ of which India 5.55 5.70 5.70 105.53 106.36 105.14 1.29 1.25

~ of which China 16.65 16.86 16.47

Total world 103.84 104.29 104.34

Source- OPEC monthly report, August 2025

Global petroleum product prices

USGC refining margins against WTI reached a 16-month high in July. Tighter middle distillate balances in

the USGC amid historically low diesel inventories and diesel production constraints exerted upward

pressure on diesel/gasoil prices and crack spreads. These dynamics positioned diesel as the main margin

driver in July. The resulting rise in diesel/gasoil margins likely contributed to a call for higher diesel yields

at the cost of that for jet/kerosene. This, coupled with healthy air travel activities over the summer season

and the subsequent uptick in jet/kerosene demand, likely contributed to higher jet/kerosene margins in

the Atlantic Basin. Additionally, slight naphtha and gasoline gains further contributed to the upturn in July

USGC refining margins. According to preliminary data, refinery intake in the USGC remained nearly flat

and added only 10 tb/d to the previous month’s level, to average 17.24 mb/d in July. USGC margins against

WTI averaged $20.62/b in July, up by $3.57, m-o-m, and up by $6.29, y-o-y.

Refinery margins in Rotterdam against Brent jumped and exhibited the largest m-o-m increase compared

to other key trading hubs. This was possibly a result of the EU’s 18th package of sanctions against Russia,

as secondary sources reported possible signs of trade disruptions for Russian products. According to

Vortexa, Russia’s oil product exports declined in July to their lowest level in nine months amid reduced

refinery rates and a spike in domestic summer demand. Vortexa data also showed refined fuel flows falling

4%, m-o-m, to 2.1 mb/d.

August 2025 Page | 33