Page 30 - Policy Economic Report_Jan 25

P. 30

POLICY AND ECONOMIC REPORT

OIL & GAS MARKET

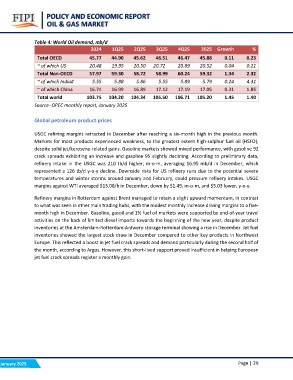

Table 4: World Oil demand, mb/d 2Q25 3Q25 4Q25 2025 Growth %

2024 1Q25

46.51 46.47 45.88 0.11 0.23

Total OECD 45.77 44.90 45.62 20.72 20.89 20.52 0.04 0.21

58.99 60.24 59.32 1.34 2.32

~ of which US 20.48 19.95 20.50 5.79 0.24 4.31

5.55 5.89 17.05 0.31 1.85

Total Non-OECD 57.97 59.30 58.72 17.12 17.19 105.20 1.45 1.40

105.50 106.71

~ of which India# 5.55 5.88 5.86

~ of which China 16.74 16.99 16.89

Total world 103.75 104.20 104.34

Source- OPEC monthly report, January 2025

Global petroleum product prices

USGC refining margins retracted in December after reaching a six-month high in the previous month.

Markets for most products experienced weakness, to the greatest extent high-sulphur fuel oil (HSFO),

despite solid jet/kerosene-related gains. Gasoline markets showed mixed performance, with gasoline 92

crack spreads exhibiting an increase and gasoline 95 slightly declining. According to preliminary data,

refinery intake in the USGC was 210 tb/d higher, m-o-m, averaging 16.95 mb/d in December, which

represented a 126 tb/d y-o-y decline. Downside risks for US refinery runs due to the potential severe

temperatures and winter storms around January and February, could pressure refinery intakes. USGC

margins against WTI averaged $13.00/b in December, down by $1.49, m-o-m, and $5.03 lower, y-o-y.

Refinery margins in Rotterdam against Brent managed to retain a slight upward momentum, in contrast

to what was seen in other main trading hubs, with the modest monthly increase driving margins to a five-

month high in December. Gasoline, gasoil and 1% fuel oil markets were supported by end-of-year travel

activities on the back of limited diesel imports towards the beginning of the new year, despite product

inventories at the Amsterdam-Rotterdam-Antwerp storage terminal showing a rise in December. Jet fuel

inventories showed the largest stock draw in December compared to other key products in Northwest

Europe. This reflected a boost in jet fuel crack spreads and demand particularly during the second half of

the month, according to Argus. However, this short-lived support proved insufficient in helping European

jet fuel crack spreads register a monthly gain.

January 2025 Page | 29