Page 30 - FIPI - Policy Economic Report - May 2025

P. 30

POLICY AND ECONOMIC REPORT

OIL & GAS MARKET

Table 4: World Oil demand, mb/d

2024 1Q25 2Q25 3Q25 4Q25 2025 Growth %

Total OECD 45.66 45.16 45.48 46.31 46.08 45.76 0.10 0.23

20.40 20.67 20.72 20.51 0.09 0.43

~ of which US 20.42 20.23 58.77 59.08 60.10 59.24 1.19 2.05

Total Non-OECD 58.05 58.98 5.84 5.50 5.91 5.74 0.19 3.39

16.68 17.03 17.04 16.90 0.25 1.50

~ of which India# 5.55 5.70 104.26 105.39 106.19 105.00 1.30 1.25

~ of which China 16.65 16.86

Total world 103.70 104.14

Source- OPEC monthly report, May 2025

Global petroleum product prices

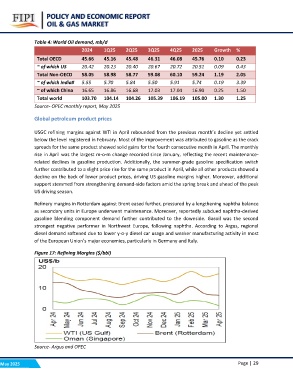

USGC refining margins against WTI in April rebounded from the previous month’s decline yet settled

below the level registered in February. Most of the improvement was attributed to gasoline as the crack

spreads for the same product showed solid gains for the fourth consecutive month in April. The monthly

rise in April was the largest m-o-m change recorded since January, reflecting the recent maintenance-

related declines in gasoline production. Additionally, the summer-grade gasoline specification switch

further contributed to a slight price rise for the same product in April, while all other products showed a

decline on the back of lower product prices, driving US gasoline margins higher. Moreover, additional

support stemmed from strengthening demand-side factors amid the spring break and ahead of the peak

US driving season.

Refinery margins in Rotterdam against Brent eased further, pressured by a lengthening naphtha balance

as secondary units in Europe underwent maintenance. Moreover, reportedly subdued naphtha-derived

gasoline blending component demand further contributed to the downside. Gasoil was the second

strongest negative performer in Northwest Europe, following naphtha. According to Argus, regional

diesel demand softened due to lower y-o-y diesel car usage and weaker manufacturing activity in most

of the European Union’s major economies, particularly in Germany and Italy.

Figure 17: Refining Margins ($/bbl)

Source- Argus and OPEC

May 2025 Page | 29