Page 31 - FIPI - Policy Economic Report - May 2025

P. 31

POLICY AND ECONOMIC REPORT

OIL & GAS MARKET

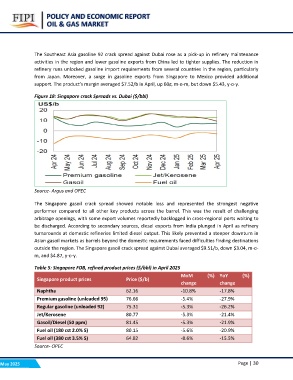

The Southeast Asia gasoline 92 crack spread against Dubai rose as a pick-up in refinery maintenance

activities in the region and lower gasoline exports from China led to tighter supplies. The reduction in

refinery runs unlocked gasoline import requirements from several countries in the region, particularly

from Japan. Moreover, a surge in gasoline exports from Singapore to Mexico provided additional

support. The product’s margin averaged $7.52/b in April, up 60?, m-o-m, but down $5.43, y-o-y.

Figure 18: Singapore crack Spreads vs. Dubai ($/bbl)

Source- Argus and OPEC

The Singapore gasoil crack spread showed notable loss and represented the strongest negative

performer compared to all other key products across the barrel. This was the result of challenging

arbitrage openings, with some export volumes reportedly backlogged in cross-regional ports waiting to

be discharged. According to secondary sources, diesel exports from India plunged in April as refinery

turnarounds at domestic refineries limited diesel output. This likely prevented a steeper downturn in

Asian gasoil markets as barrels beyond the domestic requirements faced difficulties finding destinations

outside the region. The Singapore gasoil crack spread against Dubai averaged $9.51/b, down $3.04, m-o-

m, and $4.87, y-o-y.

Table 5: Singapore FOB, refined product prices ($/bbl) in April 2025

Singapore product prices Price ($/b) MoM (%) YoY (%)

change change

-17.8%

Naphtha 62.16 -10.8% -27.9%

-26.2%

Premium gasoline (unleaded 95) 76.66 -5.4% -21.4%

-21.9%

Regular gasoline (unleaded 92) 75.31 -5.3% -20.9%

-15.5%

Jet/Kerosene 80.77 -5.3%

Gasoil/Diesel (50 ppm) 81.45 -5.3%

Fuel oil (180 cst 2.0% S) 80.15 -5.6%

Fuel oil (380 cst 3.5% S) 64.82 -8.6%

Source- OPEC

May 2025 Page | 30