Page 43 - FIPI - Policy & Economic Report May 2026

P. 43

POLICY AND ECONOMIC REPORT

OIL & GAS MARKET

Oil demand situation

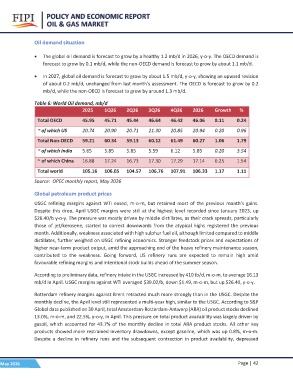

? The global oil demand is forecast to grow by a healthy 1.2 mb/d in 2026, y-o-y. The OECD demand is

forecast to grow by 0.1 mb/d, while the non-OECD demand is forecast to grow by about 1.1 mb/d.

? In 2027, global oil demand is forecast to grow by about 1.5 mb/d, y-o-y, showing an upward revision

of about 0.2 mb/d, unchanged from last month’s assessment. The OECD is forecast to grow by 0.2

mb/d, while the non-OECD is forecast to grow by around 1.3 mb/d.

Table 6: World Oil demand, mb/d 2Q26 3Q26 4Q26 2026 Growth %

2025 1Q26 46.64 46.42 46.06 0.11 0.24

21.30 20.85 20.94 0.20 0.96

Total OECD 45.95 45.71 45.44 60.12 61.49 60.27 1.06 1.79

5.59 6.12 5.85 0.20 3.54

~ of which US 20.74 20.90 20.71 17.30 17.29 17.14 0.25 1.54

106.76 107.91 106.33 1.17 1.11

Total Non-OECD 59.21 60.34 59.13

~ of which India 5.65 5.85 5.85

~ of which China 16.88 17.24 16.73

Total world 105.16 106.05 104.57

Source: OPEC monthly report, May 2026

Global petroleum product prices

USGC refining margins against WTI eased, m-o-m, but retained most of the previous month’s gains.

Despite this drop, April USGC margins were still at the highest level recorded since January 2023, up

$26.40/b y-o-y. The pressure was mostly driven by middle distillates, as their crack spreads, particularly

those of jet/kerosene, started to correct downwards from the atypical highs registered the previous

month. Additionally, weakness associated with high sulphur fuel oil, although limited compared to middle

distillates, further weighed on USGC refining economics. Stronger feedstock prices and expectations of

higher near-term product output, amid the approaching end of the heavy refinery maintenance season,

contributed to the weakness. Going forward, US refinery runs are expected to remain high amid

favourable refining margins and intentional stock builds ahead of the summer season.

According to preliminary data, refinery intake in the USGC increased by 410 tb/d, m-o-m, to average 16.13

mb/d in April. USGC margins against WTI averaged $39.02/b, down $1.49, m-o-m, but up $26.40, y-o-y.

Rotterdam refinery margins against Brent retracted much more strongly than in the USGC. Despite the

monthly decline, the April level still represented a multi-year high, similar to the USGC. According to S&P

Global data published on 30 April, total Amsterdam-Rotterdam-Antwerp (ARA) oil product stocks declined

13.0%, m-o-m, and 22.5%, y-o-y, in April. This pressure on total product availability was largely driven by

gasoil, which accounted for 43.7% of the monthly decline in total ARA product stocks. All other key

products showed more restrained inventory drawdowns, except gasoline, which was up 0.8%, m-o-m.

Despite a decline in refinery runs and the subsequent contraction in product availability, depressed

May 2026 Page | 42