Page 32 - Policy Economic Report - April 2025

P. 32

POLICY AND ECONOMIC REPORT

OIL & GAS MARKET

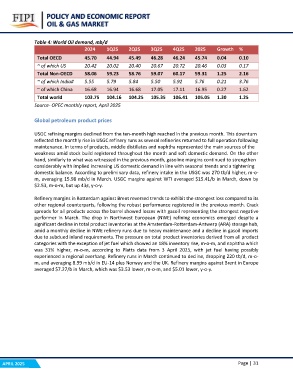

Table 4: World Oil demand, mb/d 2Q25 3Q25 4Q25 2025 Growth %

2024 1Q25 45.49 46.28 46.24 45.74 0.04 0.10

20.40 20.67 20.72 20.46 0.03 0.17

Total OECD 45.70 44.94 58.76 59.07 60.17 59.31 1.25 2.16

5.84 5.50 5.92 5.76 0.21 3.76

~ of which US 20.42 20.02 16.68 17.05 17.11 16.95 0.27 1.62

Total Non-OECD 58.06 59.23 104.25 105.35 106.41 105.05 1.30 1.25

~ of which India# 5.55 5.79

~ of which China 16.68 16.94

Total world 103.75 104.16

Source- OPEC monthly report, April 2025

Global petroleum product prices

USGC refining margins declined from the ten-month high reached in the previous month. This downturn

reflected the monthly rise in USGC refinery runs as several refineries returned to full operation following

maintenance. In terms of products, middle distillates and naphtha represented the main sources of the

weakness amid stock build registered throughout the month and soft domestic demand. On the other

hand, similarly to what was witnessed in the previous month, gasoline margins continued to strengthen

considerably with implied increasing US domestic demand in line with seasonal trends and a tightening

domestic balance. According to preliminary data, refinery intake in the USGC was 270 tb/d higher, m-o-

m, averaging 15.98 mb/d in March. USGC margins against WTI averaged $15.41/b in March, down by

$2.53, m-o-m, but up 43?, y-o-y.

Refinery margins in Rotterdam against Brent reversed trends to exhibit the strongest loss compared to its

other regional counterparts, following the robust performance registered in the previous month. Crack

spreads for all products across the barrel showed losses with gasoil representing the strongest negative

performer in March. The drop in Northwest European (NWE) refining economics emerged despite a

significant decline in total product inventories at the Amsterdam-Rotterdam-Antwerp (ARA) storage hub,

amid a monthly decline in NWE refinery runs due to heavy maintenance and a decline in gasoil imports

due to subdued inland requirements. The pressure on total product inventories derived from all product

categories with the exception of jet fuel which showed an 18% inventory rise, m-o-m, and naphtha which

was 31% higher, m-o-m, according to Platts data from 3 April 2025, with jet fuel having possibly

experienced a regional overhang. Refinery runs in March continued to decline, dropping 220 tb/d, m-o-

m, and averaging 8.99 mb/d in EU-14 plus Norway and the UK. Refinery margins against Brent in Europe

averaged $7.27/b in March, which was $3.53 lower, m-o-m, and $5.01 lower, y-o-y.

APRIL 2025 Page | 31